As global financial market volatility expands, the eyes of investors around the world are turning to Tokyo ahead of the Bank of Japan's (BOJ) monetary policy meeting scheduled for June 15-16.

Executive Summary

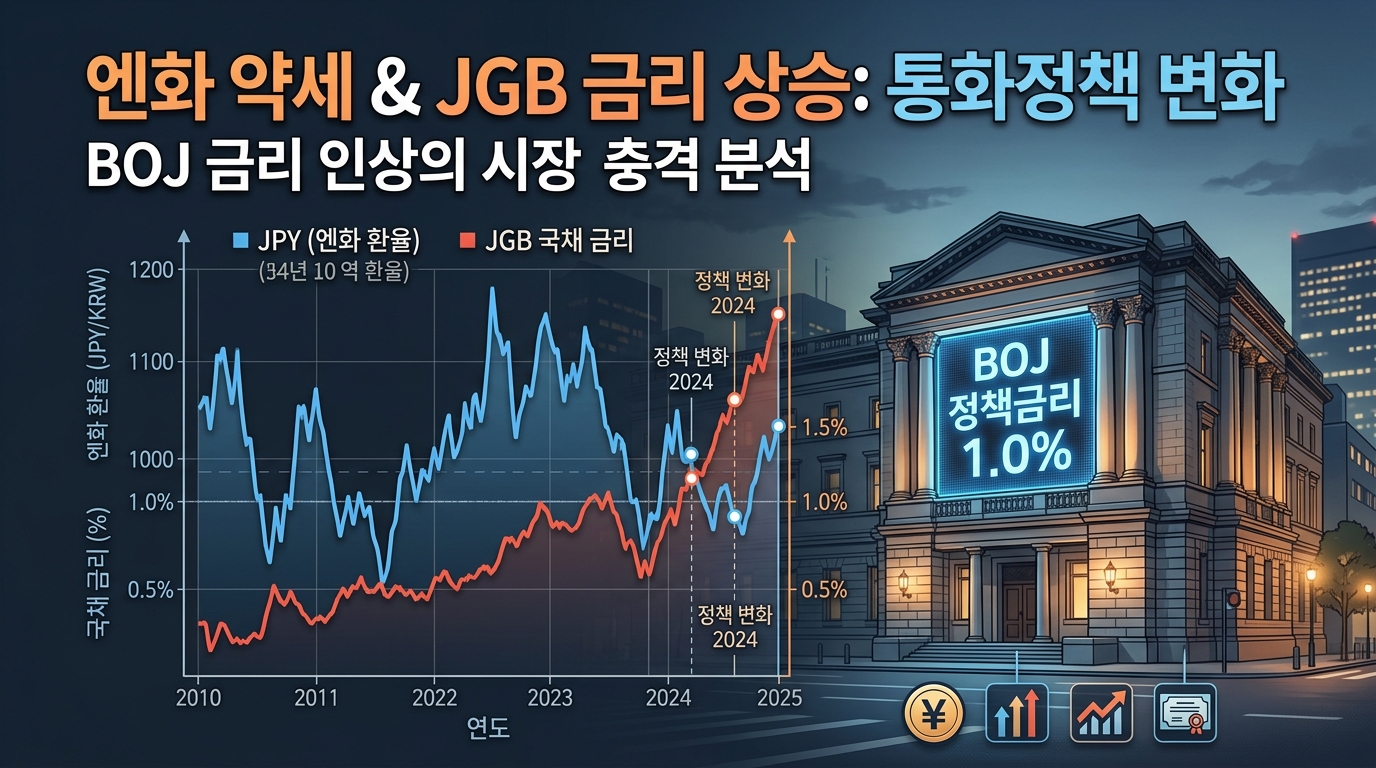

- The Bank of Japan (BOJ), led by Governor Kazuo Ueda, is widely expected to raise its benchmark interest rate by 0.25 percentage points from the current 0.75% to 1.0% at its June monetary policy meeting. This is a historic turning point, marking the first time since 1995 (approximately 31 years) that Japan's policy rate has entered the 1.0% range.

- Regarding the Japanese Government Bond (JGB) purchase reduction (tapering) plan—which has been pursued since the abolition of the Yield Curve Control (YCC) policy, once a symbol of Abenomics—a strong scenario is emerging to temporarily pause further reductions after April 2027 and maintain the current purchase pace to stabilize the bond market.

[Image: /stdaily/uploads/202606/gen_6a29b4884e4959.13209026.png]

Current Status Summary

As of intraday June 11, 2026 (tentative), global stock markets are showing an increasingly distinct pattern of fundamental decoupling among the US, Europe, and Asia.

Amid signals of prolonged tightening from some US Federal Reserve officials and hawkish moves by the European Central Bank (ECB) to counter inflation, the Bank of Japan is also signaling its transformation into a full-fledged "inflation fighter."

In particular, amid ongoing Middle East instability and Iran tensions, international oil prices have risen, increasing import price pressures in Japan. With the USD/JPY exchange rate hovering around the 160 yen mark, the prolonged weakness of the yen has made the BOJ's preemptive monetary tightening an unavoidable choice.

On the same day, the domestic stock market recorded KOSPI at 7,730.82 and KOSDAQ at 951.63, while the USD/KRW exchange rate stood at 1,519.70 won, with the Korean won also under significant weakening pressure.

With the Nasdaq index struggling intraday around the 25,657.29 level, according to Daily Stock's proprietary Fear & Greed Index, the KOSPI is currently in the "Fear" stage (31.1) and the Nasdaq is also in the "Fear" stage (33.7), indicating that global investment sentiment has weakened significantly.

Financial Analysis

Looking at Japan's macro-financial environment and the supply and demand structure of the JGB market, a delicate tightrope walk is underway between fiscal burdens from bond yield volatility and monetary normalization.

On May 18, the 10-year JGB yield soared to 2.8% per annum, reaching its highest level in about 29 and a half years, representing the reality of a market free from artificial yield suppression (YCC).

With a continuous stream of maturing government bonds currently held by the BOJ, implementing quantitative tightening (QT) faster than the market expects could trigger additional tantrums in the bond market.

| Key Indicator | June 2026 Status & Outlook | Key Characteristics & Impact |

|---|---|---|

| **Short-term Policy Rate** | 0.75% -> 1.00% (Outlook) | Likely to enter the highest level since 1995 (31 years) |

| **10-Year JGB Yield** | Volatility increased after hitting a high of 2.8% in May | Upward pressure on bond yields due to supply-demand autonomy post-YCC abolition |

| **JGB Purchase Volume** | Converging to approx. 2.1 trillion yen per month | Discussions underway to ease further tapering to curb JGB market volatility |

| **Consumer Price Index (CPI)** | 2.8% as of April (excluding gov subsidy effects) | Reflects geopolitical risks from the Middle East and accumulated weak yen effects |

[Image: /stdaily/uploads/202606/gen_6a29b495e51ee7.71597953.png]

Valuation

Comparing the relative valuation strengths of the three major global regions (US, Europe, and Asia), differences in monetary policy are significantly dividing asset attractiveness.

US equities maintain a high premium driven by robust AI infrastructure investment demand, but are undergoing multiple adjustments due to concerns over prolonged tightening. In the Eurozone, the ECB's hawkish stance limits the index's upside amid complex stagflation concerns.

Asian markets, including Japan, have absorbed global capital thanks to ultra-low interest rates and a weak yen. However, if the benchmark interest rate reaches 1.0% and pressure to unwind yen carry trades intensifies, multiple adjustments and a re-rating of index valuations may be inevitable.

In particular, with intervention vigilance near the 160 yen USD/JPY resistance level and a rising discount rate due to climbing long-term JGB yields, the relative attractiveness of the Asian region is assessed to have entered a transitional phase.

Expert and Institutional Analysis

Global investment banks (IBs) and market experts are putting weight on the possibility that the BOJ will choose a balanced strategy of "rate hikes" and "adjusting the pace of JGB purchases" at this June meeting.

According to a Bloomberg survey of economists, 49 out of 51 respondents predicted that the policy rate would be raised to 1.0% at the June meeting, presenting a scenario where it reaches 1.25% by the end of the year.

Naomi Muguruma, chief strategist at Mitsubishi UFJ Morgan Stanley Securities, analyzed, "The key point to watch is whether Governor Ueda will reveal his hawkish identity as a full-fledged 'inflation fighter' beyond simple normalization of accommodative policy."

In addition, Hideo Hayakawa, a former BOJ executive director, noted in a recent interview, "Inflationary pressures are mounting due to US tariff variables and the Japanese government's budget formulation, and the BOJ needs to accelerate its response preemptively to maintain market trust."

Risk Factors

The biggest external risk is the concern over a secondary rise in prices (cost-push inflation) of major raw materials such as crude oil and copper, driven by escalating military tensions in the Middle East.

Given the structure of the Japanese economy, which is highly dependent on energy imports, inflation caused by supply chain disruptions could reduce household real income and deepen domestic consumption stagnation, exerting downward pressure on the economy.

Furthermore, fiscal expansion plans, such as the supplementary budget aimed at economic stimulus by Prime Minister Sanae Takaichi's administration, are pointed out as policy misalignment risks that could offset the BOJ's monetary tightening effects and add upward pressure on JGB yields.

Lastly, as Japan's benchmark interest rate reaches the 1.0% range, a 31-year high, a rapid unwinding of yen carry trade funds embedded in global financial assets could amplify volatility in emerging markets and global stock markets.

[Image: /stdaily/uploads/202606/gen_6a29b4a11b46d6.92818788.png]

Investment Perspective Summary

Moving forward, the Bank of Japan's actions will serve as an important milestone reshaping the liquidity environment of Asian stock markets amid the three-way global decoupling.

Rather than focusing solely on whether a 0.25 percentage point rate hike occurs, investors should watch whether fine-tuning measures—such as pausing (maintaining) JGB purchase reduction plans after April 2027—are announced to stabilize JGB market supply and demand.

If the BOJ chooses to temporarily halt tapering to prioritize bond market protection, a rapid strengthening of the yen may be limited, but a phase vulnerable to long-term inflationary pressures and commodity-driven price volatility could be prolonged.

As global asset market sentiment remains in the fear stage, a conservative approach that prioritizes risk management—such as split positioning into yen assets and Asian stock markets during this period of macroeconomic transition—seems appropriate.

Investor Checklist Q&A

Q1. What is the probability that the Bank of Japan will actually raise its benchmark interest rate at this June meeting?

- Currently, more than 90% of economic analysts and bond strategists take a 0.25 percentage point hike for granted. If raised, the short-term policy rate will increase from the current 0.75% to 1.0%.

Q2. Since the YCC policy has already ended, why is there discussion of pausing JGB purchase reductions (tapering)?

- Although YCC, which artificially capped 10-year yields, has been abolished, long-term yields spiked excessively (recently touching 2.8%) as the BOJ reduced its JGB holdings. This raised concerns about a contraction in the domestic bond market, leading to discussions on market-protective moves to pause further reductions and adjust the pace.

Q3. Will the yen turn extremely strong once the policy rate reaches the 1.0% level?

- While interest rate hikes are typically bullish for the yen, if the BOJ mixes in accommodative policies—such as halting tapering to stabilize JGB supply and demand—upward pressure on the yen may be offset, raising the possibility that USD/JPY will move sideways near the 160 yen mark for the time being.

Q4. What is the impact of the yen carry trade unwinding on the South Korean KOSPI market?

- Global funds that previously borrowed cheap yen to invest in risky assets such as emerging market equities may be partially withdrawn due to rising interest rates in Japan. In the short term, this is a factor that could trigger foreign capital outflows and intraday volatility in emerging markets like the KOSPI.

Q5. What external indicators should investors monitor together to predict the BOJ's future path?

- Investors should comprehensively monitor international oil price trends linked to geopolitical risks in the Middle East, manufacturing PMI indicators across the US, Europe, and Asia, and the US Federal Reserve's higher-for-longer interest rate stance.