Recent adjustments to the GDPNow estimate, a key indicator showing real-time economic growth in the U.S., are drawing close attention from financial markets.

[Image: /stdaily/uploads/202606/gen_6a221fd626ef93.42154842.png]

Executive Summary

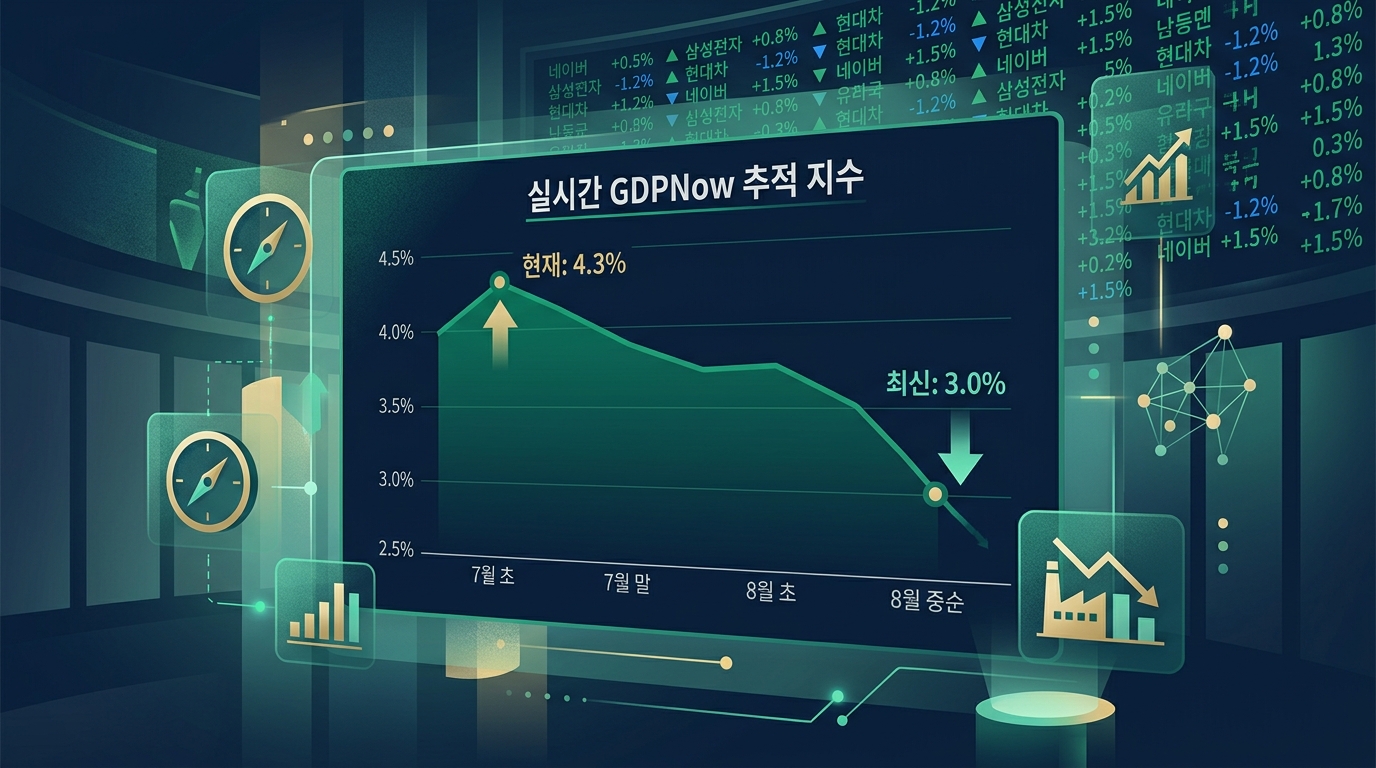

- **GDPNow Estimate Adjustment**: The Federal Reserve Bank of Atlanta's Q2 GDPNow estimate was revised downward to 3.0% (as of June 1) from its previous 4.3% (as of May 21).

- **Slowing Consumption Indicators**: The main catalyst for this downward revision is the real personal consumption expenditures (PCE) forecast lowering from 2.6% to 2.4%.

- **Resilient Manufacturing Data**: Conversely, the May ISM manufacturing index came in at 54.0, beating the expectation of 53.0 and maintaining expansionary territory, reflecting mixed economic signals.

- **Market Response**: While rate-cut expectations and slowdown concerns coexist, the Nasdaq fluctuates around the 26,830.96 mark in intraday trading.

---

Current Status Summary

As of June 1, 2026, GDPNow—the Federal Reserve Bank of Atlanta's real-time Q2 GDP estimation model—forecasted a growth rate of 3.0%.

This is a notable moderation compared to the 4.3% projection recorded in mid-May, reflecting a recent slowdown in U.S. consumer spending trends.

Nonetheless, this figure still suggests that rebound momentum remains intact when compared to the final Q1 real GDP growth rate of 1.6%.

Market participants interpret this as a factor that could ease concerns about high interest rates staying elevated for longer due to an overheating economy, while remaining cautious about whether slowing consumption could lead to a recession.

---

Financial Analysis

Breaking down the details of the GDPNow model shows that forecasts for both real personal consumption expenditures (PCE) growth and real gross private domestic investment (GPDI)—key gauges of the domestic U.S. market—were adjusted downward simultaneously.

Following the release of leading economic indicators from the Department of Commerce, the real PCE growth forecast was revised down from 2.6% to 2.4%, and the GPDI forecast dropped from 10.4% to 9.3%.

| Indicator | May 21 Forecast | May 28 Forecast | June 1 Forecast |

|---|---|---|---|

| **GDPNow Real GDP Growth** | 4.3% | 3.8% | 3.0% |

| **Real Personal Consumption Expenditures (PCE)** | 2.9% | 2.6% | 2.4% |

| **Real Gross Private Domestic Investment (GPDI)** | 11.4% | 10.4% | 9.3% |

In contrast, the May manufacturing PMI released by the Institute for Supply Management (ISM) posted 54.0, staying in expansion territory above 50 for the fifth consecutive month.

In particular, the New Orders Index (56.8) and the Production Index (54.3) remained strong, proving that AI infrastructure rollouts and domestic manufacturing reshoring effects are still robust.

---

Valuation

The U.S. stock market is currently recalibrating valuations as it balances confidence in a soft landing against changes in the interest rate outlook.

[Image: /stdaily/uploads/202606/gen_6a221fe3830640.36223500.png]

The Nasdaq Index hovered in a tight balance, pointing to 26,830.96 in intraday trading as of June 5, 2026 (provisional).

At the same time, the domestic KOSPI index was at 8,102.80 and the KOSDAQ was at 998.54 during intraday trading, while the USD/KRW exchange rate remained at 1,540.10 KRW, maintaining dollar strength pressure.

According to Daily Stock's proprietary Fear & Greed Index, the Nasdaq is currently at a Neutral level (54.7), cooling off from its Greedy state (60.1) a week ago to enter a more stable phase.

The KOSPI's Fear & Greed Index also remains Neutral (47.8), indicating that market participants are increasingly taking a wait-and-see approach.

---

Expert & Institutional Analysis

Economic forecasts from global investment banks and major regional Feds present a somewhat mixed and complex picture.

For instance, the New York Fed's "Staff Nowcast" model predicts Q2 real GDP growth at 2.5%, taking a more conservative stance than the Atlanta Fed's GDPNow (3.0%).

New York Fed economists stated, "While there was a positive impact from newly updated manufacturing new orders data, it was partially offset by weakening growth in personal consumption."

Some academic experts suggest a scenario where further downward revisions to consumption indicators could accelerate the Fed's rate-cut pace in the second half of the year.

However, the Prices Paid Index within the manufacturing PMI remains elevated at 82.1, prompting cautious views that high inflation concerns could hinder rate cuts.

---

Risk Factors

The key risks that investors need to watch closely include the potential for a sharp cooling of the real economy.

First, there is the possibility of a "consumption cliff," where personal consumption—which has been the economy's backbone—weakens rapidly due to depleted household savings and the cumulative burden of high interest rates.

Second, if oil prices remain high due to geopolitical tensions (such as conflicts in Iran), rising energy costs could directly squeeze corporate profit margins.

Third, there is the concern of stagflation, where inflation metrics do not fall as quickly as expected due to structurally rising manufacturing costs driven by the reshoring and AI investment booms.

---

Investment Perspective

An economic path where growth moderates appropriately (around the 3.0% level) without a sharp downturn can provide a long-term positive "Goldilocks" environment for the stock market.

However, if the slowdown in consumption momentum exceeds expectations, downward pressure on earnings estimates for sectors like consumer discretionary within the S&P 500 will intensify.

Conversely, industrials and technology sectors, buoyed by ongoing infrastructure investments, are highly likely to exhibit strong downside support.

Therefore, at this juncture, a diversification strategy that balances value and growth stocks in portfolios to manage risk seems more favorable than aggressively chasing the broader indexes.

---

Investment Checklist

Here are 5 key checkpoints to verify before making investment decisions:

- **Further Downward Revisions to Q2 GDPNow**: Track whether the Atlanta Fed's final Q2 GDP estimate slips below the mid-2% range.

- **Recovery Trends in Consumption Data**: Analyze whether the monthly real personal consumption expenditures (PCE) and retail sales indicators are bottoming out.

- **Decline in PMI Prices Paid**: Monitor whether the prices paid sub-index of the manufacturing PMI stabilizes below the 80 level.

- **Changes in the Nasdaq Fear & Greed Index**: Watch whether the index, currently sitting at Neutral (54.7), heats up back into Greed or slides down into Fear.

- **Exchange Rate Volatility**: As the USD/KRW exchange rate remains high at 1,540.10 KRW, check whether the strong dollar trend triggers capital outflows from emerging markets.