Hello. This is Daily Stock.

Summary

- While the KRW/USD exchange rate has settled in the 1,500 won range, an unusual decoupling phenomenon continues, where South Korea's June exports surpassed $100 billion for the first time but the high exchange rate persists.

- As rising shipbuilding prices and the weakening won combine to bring the "real Korean won shipbuilding price" close to an all-time high, the shipbuilding sector, which has a high portion of dollar settlements, is emerging as a major beneficiary among large-cap stocks.

- For HD Hyundai Heavy Industries (329180), the integration effects with HD Hyundai Mipo, revenue recognition of high-value LNG carriers, and favorable exchange rate effects are combining to highly increase the likelihood of a significant improvement in operating profit for Q2 2026.

Current Market Status

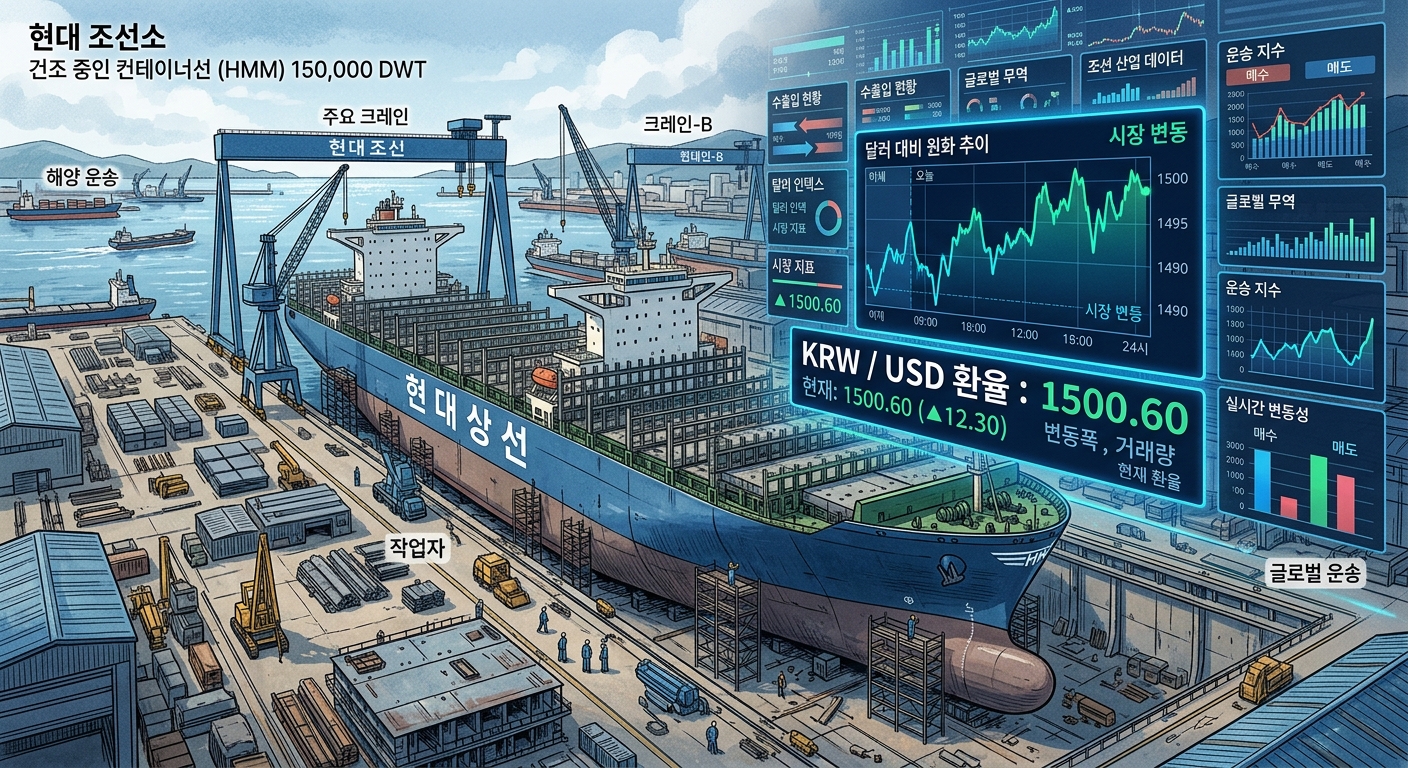

As of the market close on July 8, 2026, the KOSPI index closed at 7,246.79 points, and the KRW/USD exchange rate finished at 1,500.60 won.

In South Korea's economy recently, export volume in June reached $102.25 billion, surpassing the $100 billion monthly threshold for the first time in history. However, the exchange rate has maintained its ultra-high level in the 1,500 won range over the long term.

This unusual decoupling phenomenon is interpreted as the result of unresolved imbalances in dollar supply and demand in the foreign exchange market and persistent global geopolitical instability.

In this environment of exchange rate volatility holding above the 1,500 won level, the "K-Shipbuilding" sector—characterized by a high proportion of dollar settlements and maximized won-converted profits—is attracting attention as a strong defensive play among KOSPI large-caps.

Currently, the KOSPI Fear & Greed Index compiled by Daily Stock stands at "Extreme Fear (12.5)," showing a sharp decline in market sentiment compared to one week ago (34.3) and one month ago (31.4).

Conversely, the Nasdaq Fear & Greed Index is currently at a "Neutral (43.5)" level, suggesting that investment sentiment in the domestic stock market is taking a much more conservative path.

[Image: /stdaily/uploads/202607/gen_6a4df5c2baf253.24905483.png]

Financial Analysis

Among major shipbuilding large-cap stocks, HD Hyundai Heavy Industries' (329180) financial trajectory for the first half of 2026 shows a steep upward trend.

Following its Q1 performance, where it recorded revenue of 5.9 trillion won and operating profit of 905 billion won—beating the market consensus by 2% and 14%, respectively—the company is expected to sustain this momentum into the second quarter.

According to security industry estimates, HD Hyundai Heavy Industries' Q2 2026 consolidated revenue is projected to rise 50.9% year-on-year to 6.2601 trillion won, with operating profit climbing 105.7% to 969.6 billion won (operating profit margin of 15.5%).

The fundamental driver of these robust earnings is the official revenue recognition from building eco-friendly and LNG carriers secured during past high-price periods.

Additionally, synergies from the integration of HD Hyundai Mipo late last year, sustained high profitability in the engine business division, and process optimization through smart yard solutions are all contributing positively.

| Classification | 2024 (Actual) | 2025 (Preliminary/Est.) | 2026 (Forecast) |

|---|---|---|---|

| **Revenue (Billion KRW)** | 14,486.5 | 17,580.6 | 23,261.9 |

| **Operating Profit (Billion KRW)** | 705.2 | 2,037.5 | 3,339.2 |

| **Operating Margin (%)** | 4.9% | 11.6% | 14.4% |

| **Net Profit (Controlling Interest) (Billion KRW)** | 621.5 | 1,415.5 | 2,503.6 |

| **ROE (%)** | 11.4% | 18.8% | 24.5% |

Valuation

Having completely emerged from its historical tunnel of chronic deficits, HD Hyundai Heavy Industries' stock price has firmly entered a stable earnings recovery phase in 2026.

The valuation framework for the shipbuilding industry, which previously centered on asset values like P/B (Price-to-Book ratio), is accelerating its multiple transition toward the P/E (Price-to-Earnings) ratio, reflecting actual earnings generation capabilities.

Based on estimated 2026 EPS (Earnings Per Share), HD Hyundai Heavy Industries' P/E multiple has moderated to approximately 19.4x, justifying its stock price through fundamental performance.

Major financial institutions have recently raised their 12-month target price for HD Hyundai Heavy Industries by about 12.5% from 800,000 won to 900,000 won, maintaining a positive outlook.

The annual operating profit forecast also continues to trend slightly upward, driven by consistently favorable exchange rate conditions and the normalization of production processes.

[Image: /stdaily/uploads/202607/gen_6a4df5ce3b0367.19593562.png]

Expert & Institutional Analysis

Securities industry experts analyze that the macroeconomic environment of a prolonged weak Korean won delivers an unprecedented real ship price increase effect to domestic shipbuilders.

Although the upward momentum of the USD-denominated Newbuilding Price Index has plateaued (around 184.98pt), the KRW/USD exchange rate in the 1,500 won range raises real revenues when converted to the won, which is the currency used for cost expenditures.

For instance, when delivering a $250 million LNG vessel, a 5% rise in the exchange rate yields a direct benefit of over 20 billion won in real won-denominated contract value for the shipbuilder.

Institutional investors are particularly focusing on the fact that HD Hyundai Heavy Industries' marine engine division has secured a new growth engine in land-based power generation engines for AI data centers in North America.

This is interpreted as an opportunity for the company to transition from a simple shipbuilder to an eco-friendly power infrastructure provider addressing the global power shortage.

Risk Factors

However, a high exchange rate exceeding 1,500 won is not unconditionally positive for all exporting companies.

First is the risk of "FX hedge trigger contracts" backfiring. If smaller exporting companies have signed up for foreign exchange hedging products that cap the exchange rate under 1,500 won, they face the risk of mounting valuation losses on derivatives as the rate exceeds their expected ranges.

Nevertheless, large-scale shipbuilders like HD Hyundai Heavy Industries manage strict internal currency policies, meaning their exposure to such trigger risks is assessed as relatively low.

Second is raw material price volatility and labor shortages. Under a weak won, the price of thick steel plates, which correlates with imported iron ore prices, could rise and increase cost burdens. The shortage of skilled labor on-site and rising wage pressures also remain long-term challenges.

Investment Perspective

In an era of the "hyper-exchange rate new normal," where high exchange rates and historic export highs coexist, a selective approach focused on large caps that can secure real margins rather than simple revenue growth may be effective.

The shipbuilding sector, led by HD Hyundai Heavy Industries, has already secured more than three years' worth of backlog and is on a favorable exchange rate path, offering very high earnings visibility.

At a time when the KOSPI remains in an extreme fear phase and continues to show volatility, a long-term perspective grounded in firm earnings momentum and improvements in the high-value vessel product mix is required over short-term supply-demand fluctuations.

Investor Checklist Q&A

Q1. Why is the Korean won not strengthening despite the KRW/USD exchange rate being in the 1,500 won range?

A1. Despite a record-high current account surplus, strong dollar pressure driven by geopolitical risks and US interest rate paths continues to weigh on the won's value, perpetuating a supply-demand imbalance.

Q2. Is the rise in exchange rates immediately reflected in shipbuilding earnings?

A2. The shipbuilding industry uses a heavy-tail payment method, making the exchange rate at the time of delivery highly critical. Since the order backlog is denominated in US dollars, a higher exchange rate increases the won-equivalent value of the backlog and boosts margins upon delivery.

Q3. Could the FX hedge trigger risk become a negative factor for HD Hyundai Heavy Industries?

A3. Large shipbuilders systematically control exchange rate risks through stable forward exchange contracts, leaving them largely unaffected by KIKO-style currency loss concerns seen in some small and medium-sized firms.

Q4. Are there concerns about intensifying competition with Chinese shipyards?

A4. Although China is actively entering the high-value LNG carrier market, domestic shipbuilders maintain their position as the preferred choice for shipowners based on unrivaled eco-friendly smart vessel technology and delivery reliability.

Q5. Besides shipbuilding, which other exporting sectors benefit from the high exchange rate?

A5. Semiconductors and automobiles, which have high proportions of overseas revenue, along with power equipment benefiting from global grid investments, defense, and K-food sectors with rapidly growing exports, are major beneficiaries of the rising exchange rate.