Hello. This is Daily Stock.

[Image: /stdaily/uploads/202607/gen_6a4958b7f27f58.34313991.png]

Summary

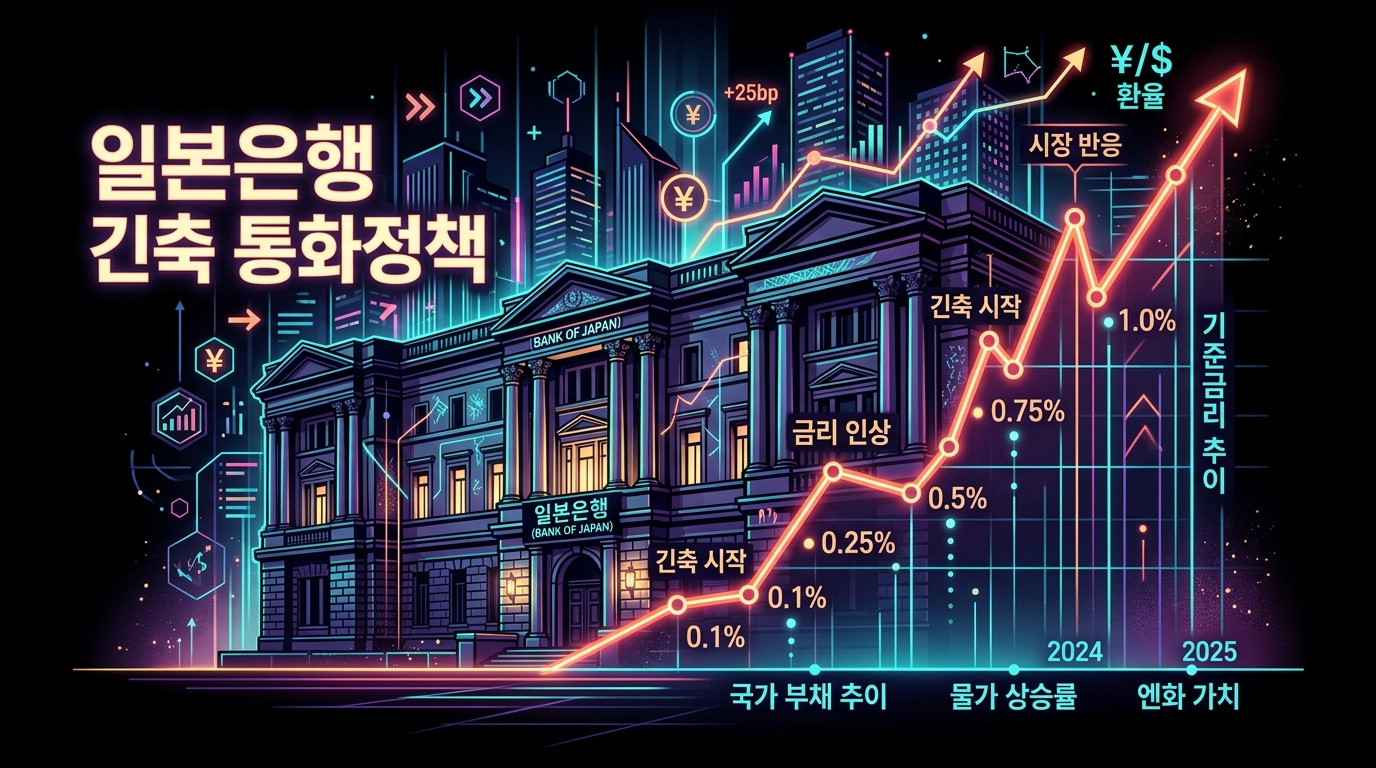

The Bank of Japan (BOJ) recently raised its benchmark interest rate by 25 basis points from 0.75% to 1.00% during its monetary policy meeting.

This marks the highest rate since September 1995, about 31 years ago, signaling the end of the Yield Curve Control (YCC) policy—a hallmark of Abenomics—and the beginning of genuine monetary normalization.

Global stock markets are seeing decoupling fundamentals across the United States, Europe, and Asia.

On the day, the domestic KOSPI closed at 8,088.34, the KOSDAQ at 868.41, and the Nasdaq at 25,832.67, reflecting both mixed sentiment and downward pressure.

According to Daily Stock’s proprietary Fear and Greed Index, the KOSPI is currently in the "Fear" stage at 21.2, compared to 35.7 (Fear) a week ago, 21.6 (Fear) a month ago, and 32 (Fear) three months ago.

This indicates that investor sentiment has remained frozen for an extended period.

Meanwhile, the Nasdaq Fear and Greed Index is at 31.9 (Fear), a sharp decline from 25.1 (Fear) last week, 53 (Neutral) a month ago, and 77.6 (Greed) three months ago.

Anxieties over tightening liquidity are dominating the market.

Market Overview

During its monetary policy meeting in June, the BOJ approved the rate hike with a 7-to-1 majority among the eight board members.

With Governor Kazuo Ueda hospitalized due to health issues, Deputy Governor Shinichi Uchida led the meeting, delivering a decision that aligned with market expectations.

The primary driver behind the rate hike is cumulative raw material cost increases driven by geopolitical tensions in regions like Iran, which have fueled inflationary pressures.

While oil prices have stabilized somewhat on prospects of a potential peace agreement between the U.S. and Iran, elevated import prices continue to stoke inflation expectations.

At the same time, the Japanese government has called for close policy coordination, citing Article 4 of the Bank of Japan Act and previous joint statements.

Prime Minister Sanae Takaichi’s administration has voiced concerns that rapid interest rate hikes could dampen domestic demand, urging the central bank to pace its actions carefully.

In the global macroeconomic landscape, the European Central Bank (ECB) raised its policy rate to 2.25% to combat stagflation, while the People's Bank of China (PBOC) maintains an expansionary stance.

With the U.S. Federal Reserve keeping interest rates higher for longer, the monetary policy paths of these three major economic blocs are decoupling further.

Financial Analysis

Following years of quantitative easing, the BOJ’s balance sheet remains massive, with its Japanese Government Bond (JGB) holdings accounting for over half of the market.

However, in 2026, the BOJ has scaled back its monthly bond purchases from approximately 5.7 trillion yen to 2.9 trillion yen, executing a de facto quantitative tightening (QT).

Real economic indicators also point to structural changes in the economy.

Japan’s core Consumer Price Index (CPI) growth projection for fiscal year 2026 is at 2.4%, consistently exceeding the BOJ’s 2.0% target.

| Key Economic Indicator | March 2024 (Negative Interest Rate Exit) | December 2025 | June 2026 (Current) | End of 2026 Forecast |

|---|---|---|---|---|

| **Short-term Policy Rate** | 0.00% – 0.10% | 0.75% | 1.00% | 1.25% |

| **Monthly JGB Purchases** | ~6.0T Yen | ~3.4T Yen | ~2.9T Yen | To be reduced further |

| **Core CPI Outlook** | 2.5% | 2.3% | 2.4% | 2.4% |

| **GDP Growth Outlook** | 0.7% | 0.5% | 0.6% | 0.6% |

[Image: /stdaily/uploads/202607/gen_6a4958c1d88629.28890028.png]

Japan’s real GDP growth forecast remains at a modest recovery pace of 0.6%.

However, weak consumer spending driven by prolonged high inflation remains a major financial concern for fiscal and monetary authorities.

Valuation

Japan's 10-year JGB yield reached its highest level in several years, hovering in the high 1.9% range, exerting direct pressure on global bond prices.

As the yield gap with U.S. Treasuries narrows, the yen's undervaluation discount is dissipating, driving a rebound in the yen's value and the KRW/JPY exchange rate.

On the day, the USD/KRW exchange rate remained elevated at 1,530.00, reflecting capital outflow pressures from emerging markets.

Conversely, rising JGB yields are beginning to act as a magnet pulling global capital back into Japan.

Comparing global index valuations highlights the undervaluation of Asian markets.

While the KOSPI remains stuck in a long-term range, trading at deeply undervalued levels relative to its asset value, the Nasdaq is easing its valuation burden through technical corrections from historic highs.

Europe, in particular, is experiencing accelerated capital outflows amid concerns over a manufacturing slowdown, shifting the center of gravity in global asset allocation.

This transition stage is seeing capital diversify away from the U.S. toward Japan and select emerging Asian markets where currency benefits are becoming more apparent.

Expert & Institutional Analysis

Global financial experts anticipate the BOJ will raise interest rates at least once more this year, reaching 1.25% by year-end.

Global investment banks, including United Overseas Bank (UOB), analyze that because this rate hike was well-telegraphed, a sudden market crash like the one seen in the summer of 2024 is unlikely to recur.

However, changes in the composition of the Monetary Policy Committee could slow down the pace of rate hikes.

Newly appointed board member Ayano Sato is considered relatively dovish, which could boost the case for a rate freeze in the third quarter.

Geopolitical risk analysts point out that if U.S. sanctions relief on Iran and diplomatic efforts stabilize commodity prices, the justification for aggressive rate hikes may weaken.

As a result, the BOJ is expected to approach further tightening with caution.

Domestic financial experts warn that even if the yen-carry trade does not unwind abruptly, there remains a risk that marginal capital deployed in emerging markets could be withdrawn.

This could increase the volatility of foreign capital flows in the Korean stock market for the time being.

Risk Factors

The most prominent risk is an unruly unwinding of the yen-carry trade, which could trigger a global asset market shock.

If funds borrowed in low-interest yen to invest in high-yield assets, such as U.S. tech stocks or emerging market bonds, are suddenly recalled, global liquidity constraints could intensify.

[Image: /stdaily/uploads/202607/gen_6a4958cab9fdc1.07900460.png]

Secondly, there is the risk of an increased interest expense burden on the Japanese government’s record-high public debt.

With JGB yields approaching 2%, the cost of servicing government debt is set to jump, potentially deteriorating fiscal health.

Lastly, global supply chain disruptions and the potential recurrence of geopolitical instability in the Middle East present risks.

If crude oil and natural gas prices surge again, the BOJ could face a dilemma where it is forced to hike rates to combat stagflationary pressures despite slowing economic growth.

Investment Outlook

As monetary policies in the U.S., Europe, and Asia continue to diverge, investors should maintain a highly diversified approach.

In the short term, the BOJ's policy normalization could strengthen the yen, potentially benefiting export-heavy domestic sectors by enhancing relative price competitiveness.

However, during periods of shrinking global liquidity, valuation adjustments across asset markets remain a strong possibility.

Consequently, close attention should be paid to the BOJ's upcoming monetary policy meeting scheduled for July 29–30, as well as the pace of its JGB purchase reductions.

Investors may want to review their exposure to currency-sensitive assets and prioritize defensive value stocks or large-cap equities with robust cash flows.

Rather than making speculative directional bets, a cautious approach that monitors policy coordination among major central banks and shifts in economic data is recommended.

Investor Checklist Q&A

Q1. What is the primary reason behind the BOJ raising its policy rate to 1.00% for the first time in 31 years?

The primary driver is cumulative import inflationary pressure, exacerbated by Middle East instability.

With inflation expectations rising and the inflation rate consistently exceeding the BOJ's 2.0% target, the central bank took preemptive action.

Q2. Will the unwinding of the yen-carry trade trigger a major crash in global stock markets?

Many experts believe a sudden market crash is unlikely because this rate hike was anticipated months in advance.

However, as capital continues to leave high-yield assets to repay yen-denominated debt, volatility in some emerging market assets could rise.

Q3. Why did Prime Minister Sanae Takaichi's administration urge caution to the BOJ?

The government is concerned that rapid rate hikes could excessively dampen domestic consumption and business investment sentiment.

Invoking Article 4 of the Bank of Japan Act, the administration has pressed the BOJ to align its monetary policy pacing with the government’s broader economic objectives.

Q4. Could a stronger yen benefit the Korean economy and the KOSPI?

Yes, a stronger yen can enhance the price competitiveness of Korean exporters, particularly in sectors like automotive and shipbuilding that compete directly with Japanese firms.

However, if this is accompanied by a rapid withdrawal of foreign capital due to tightening global liquidity, the overall index could still face downward pressure.

Q5. What are the key dates and indicators that investors should monitor next?

The BOJ's next monetary policy decision meeting on July 29–30 will be a crucial turning point.

Investors should closely analyze the detailed QT roadmap for JGB purchase reductions and the remarks of the newly appointed dovish board members to gauge the trajectory of future rate hikes.