This is Daily Stock, delivering the latest trends in the global financial market swiftly and accurately.

[Image: /stdaily/uploads/202606/gen_6a3ecc877b5e01.20880194.png]

Executive Summary

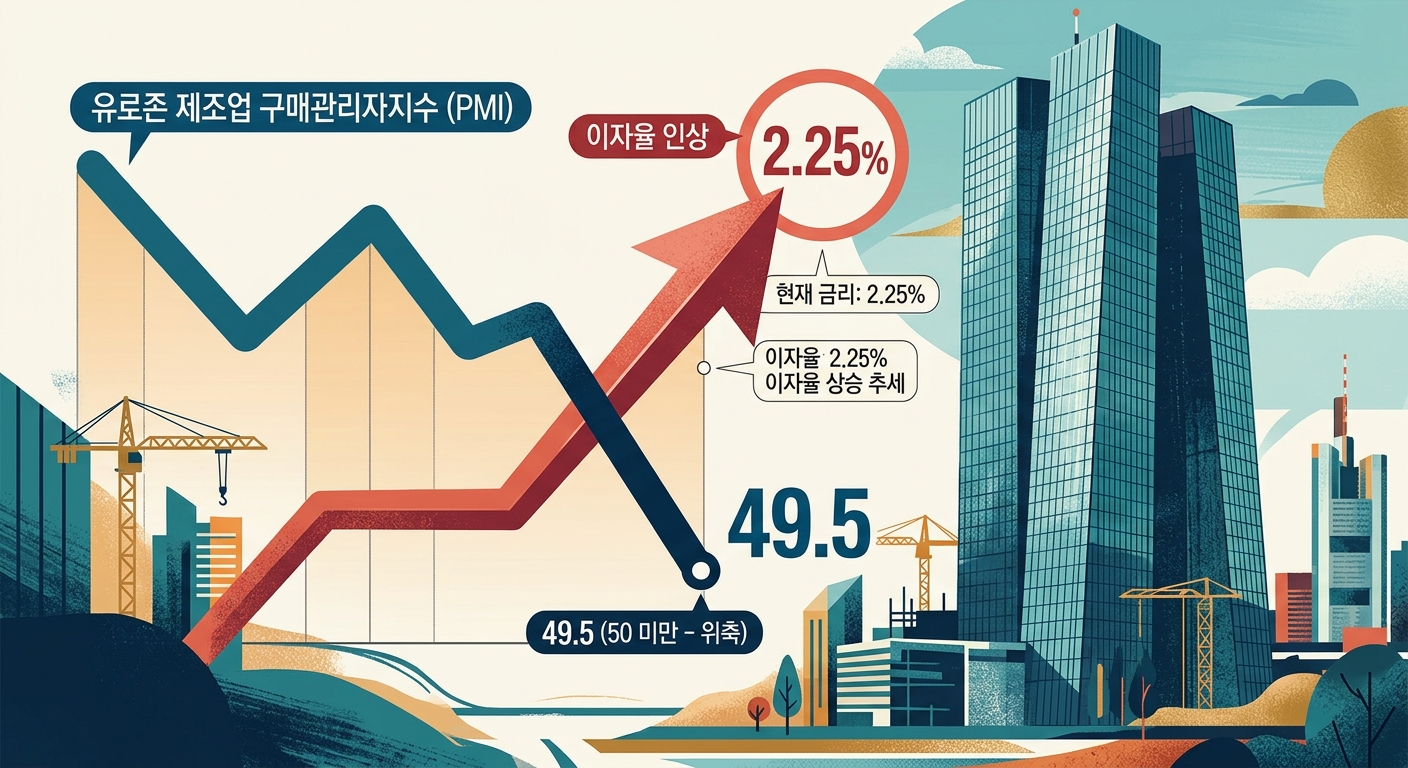

- The Eurozone's June Composite PMI rebounded to 49.5, supporting the economic recession defense line, although a growth gap between manufacturing and services is being observed.

- The European Central Bank (ECB) unexpectedly raised key interest rates by 25 basis points (bps), raising the deposit facility rate to 2.25% to counter inflation and energy price pressures stemming from Middle East conflicts.

- Amid U.S. inflation and Asia's accommodative policy stance, the Eurozone is pursuing its own tri-polar decoupling path, aiming to curb high inflation while simultaneously mounting a moderate economic defense.

Market Overview

The Eurozone economy is currently dominated by rising cost pressures from geopolitical tensions and concerns over slowing growth.

The recently released June S&P Global Eurozone Composite PMI (Purchasing Managers' Index) stood at 49.5, improving slightly from 48.5 in the previous month.

Although it remained in contraction territory for the third consecutive month by staying below the threshold of 50, it reached a three-month high, signaling that a rapid slide into a recession is being held at bay.

In particular, the services PMI rebounded to 48.9, hinting at a potential recovery in the tourism and leisure sectors.

On the other hand, the manufacturing PMI, which had been expanding, softened slightly to 51.3 from the previous month's 51.6, showing that the impact of supply chain disruptions remains.

Under these circumstances, the ECB unexpectedly raised its policy rates, including the deposit rate, by 25 bps at its monetary policy meeting held on June 11, aligning with some market forecasts.

| Key Economic Indicators / Interest Rates | May 2026 Value | June 2026 Value | Remarks |

|---|---|---|---|

| Eurozone Composite PMI | 48.5 | 49.5 | Highest level in 3 months |

| Eurozone Services PMI | 47.7 | 48.9 | Gradual improvement amid contraction |

| Eurozone Manufacturing PMI | 51.6 | 51.3 | Maintained expansion with a slight slowdown |

| ECB Deposit Facility Rate | 2.00% | 2.25% | Raised by 25 bps (effective June 17) |

| ECB Marginal Lending Rate | 2.40% | 2.65% | 25 bps hike completed |

| ECB Main Refinancing Operations (MRO) | 2.15% | 2.40% | 25 bps hike completed |

Financial Analysis

According to the ECB's June economic outlook report, the 2026 Eurozone headline inflation forecast was revised upward from 2.6% to 3.0%.

This is interpreted as a secondary pass-through of rising energy and raw material prices from the ongoing Middle East conflict into processed goods and service prices.

In contrast, the 2026 real GDP growth forecast was lowered to 0.8%, officially confirming increased downward economic pressure.

[Image: /stdaily/uploads/202606/gen_6a3ecc9179d592.74846313.png]

While short-term profitability for European companies facing cost burdens is under pressure, the moderation in input and output price growth in the June PMI survey is encouraging.

However, as prolonged high interest rate burdens increase credit costs for many marginal firms, scenarios of reduced capital expenditure and employment contraction remain key concerns.

Valuation

Amid the global tri-polar decoupling, valuation metrics such as the Price-to-Earnings (P/E) ratio of European equities (STOXX 600) reflect a substantial discount compared to U.S. equities.

However, the ECB's monetary policy stance of returning to tightening and the weak domestic demand recovery are capping multiples for European financial and manufacturing indices.

In particular, the distinct growth slowdown in Germany (DAX) and France (CAC40) acts as a discount factor for Euro-denominated assets overall.

The bond market is also pricing in some possibility of additional rate hikes, with short-to-medium-term Eurozone sovereign yields reflecting minor upward pressure.

Expert and Institutional Analysis

Global asset manager Swisscanto assessed, "Implementing additional monetary tightening when the real economy is already contracting is an inevitable choice to curb supply-shock-driven inflation, but it will add burden to the economy."

Capital Economics projected that if tensions in the Middle East and supply chain disruptions persist throughout the third quarter, the ECB could implement another 25 bps rate hike at its July meeting.

Chris Williamson, Chief Business Economist at S&P Global, placed weight on sideways growth, noting, "The recovery of the Eurozone Composite PMI to 49.5 is a positive sign of resilience to avoid falling into a technical recession."

Risk Factors

The largest risk is a scenario where energy prices surge further depending on the developments in the Middle East conflict, accelerating supply-driven inflation beyond the ECB's control.

There is also a strong concern that high-interest pressures will further dampen household consumer sentiment, extinguishing the warmth in the services sector that was just showing signs of recovery.

Lastly, unstable global and domestic financial sentiments also pose risks.

As of today, the KOSPI closed at 8,411.21 points, while the KOSDAQ closed at 851.37 points.

The U.S. Nasdaq is also hovering around 25,262.76 points.

In tandem, the KRW-USD exchange rate is showing high volatility, trading around 1,534.30 KRW.

In particular, according to the Daily Stock Fear & Greed Index, the Nasdaq Fear & Greed Index remains in the "Fear (25.6)" zone amid extreme tension.

Furthermore, the domestic KOSPI Fear & Greed Index has also slipped to the "Fear (39)" stage, indicating a chilling of investment sentiment across global assets.

Investment Outlook Summary

The rebound in the Eurozone's June PMI helped establish a psychological support line, suggesting that the worst-case recession scenario is being defended.

However, the ECB's hawkish move of raising the deposit rate to 2.25% is highly likely to restrict rapid capital flows into risk assets.

Observing the global tri-polar decoupling trend, it seems reasonable for investors to selectively approach the European market, focusing on undervalued, high-quality export stocks and defensive dividend assets.

Geopolitical stability in the Middle East and the Eurozone Consumer Price Index (CPI) trend to be released in July will serve as milestones for future asset allocation decisions.

Investor Checklist Q&A

Q1. What was the core reason for the ECB raising the deposit rate to 2.25% in June?

A1. It was driven by the upward revision of this year's Eurozone inflation forecast to 3.0% as risks of rising energy prices, such as crude oil, increased due to the Middle East conflict.

Q2. Should the Eurozone Composite PMI of 49.5 in June be viewed as a positive signal?

A2. Although still pointing to economic contraction as it is below the threshold of 50, it is interpreted as a moderately positive recovery signal that eased severe recession concerns by improving significantly from the previous month (48.5).

Q3. Compared to the U.S. Federal Reserve, what is the distinct trend shown by the ECB?

A3. Despite facing relatively higher downside economic risks, the ECB has strengthened its own preemptive tightening to prevent hyperinflation triggered by supply shocks from becoming entrenched.

Q4. Is the polarization between the European manufacturing and service sectors resolving?

A4. The manufacturing PMI (51.3) remained expansionary but softened, while the services PMI (48.9) rebounded, indicating that the gap between the two sectors is narrowing slightly.

Q5. What volatility indicators should be monitored closely when investing in European equities going forward?

A5. The general fear sentiment in the global asset markets (such as the Nasdaq Fear & Greed Index at 25.6) and whether energy spot prices stabilize downward following a potential ceasefire in the Middle East.